Visa International Service Assessment (ISA) Fee Explained

What is the Visa International Service Assessment (ISA) Fee? The Complete Merchant Guide

I know what it feels like to open that credit card processing statement. It’s like getting a bill written in ancient Greek. You see dozens of tiny charges, a few dollars here, a few cents there. It all adds up, but what are you paying for? Trying to figure out those small fees can be hard.

Often, my clients spot the phrase, “Visa International Service Assessment.” They immediately call me, asking if it is a new tax or some random hidden cost. I get it. It is confusing. This specific charge is one of the less common fees that hits U.S. merchants.

Let me make this charge clear for you. I want to define this assessment, explain exactly when it happens, detail the cost, and give you solid advice on managing it. No one should pay fees they don’t understand. This article is my way of pulling back the curtain on this particular assessment.

Here is a quick look at the vital topics I'm going to cover for you today:

Topics We Will Cover

- What this specific fee is, and why Visa charges it.

- The exact conditions that trigger the charge on my business transactions.

- The difference between the ISA Fee and the IAF Fee (they stack!).

- My total real-world cost picture for accepting a foreign card.

- The exact places and names I can use to find this charge on my monthly statement.

- Why I cannot negotiate this fee, and what I should negotiate instead.

- How other card companies handle international payments.

When Does My Business Get Charged the ISA Fee?

This charge has a very specific trigger. You will not see it on every transaction, only on certain ones.

The Core Rule: The Trigger

The Visa International Service Assessment is a charge imposed by Visa. Visa put this charge in place to help cover the added risk and cost of handling payments that cross international lines.

The fee is activated when a transaction involves these two things:

- A U.S. acquiring bank (that is my payment processor).

- A non-U.S. issuing bank (that is the customer’s bank).

That is the entire rule. It sounds simple, but it is often misunderstood.

Keep this in mind: The assessment has nothing to do with the customer's physical location. It is only about where the customer’s Visa card was first issued. If the card came from a bank outside the United States, I will pay this specific fee.

For instance, a customer could be standing right in my shop in Dallas. If their card was issued by a bank in Brazil, I pay the charge. The purchase is happening locally, but the money is moving across borders in the background. Visa charges this fee for the service of clearing that international payment.

Examples of ISA Fee Scenarios

Let me give you a few real-world examples so this is crystal clear for your business:

Example 1: The Retail Tourist I own a small gift shop near a national park in California. A visitor from France buys a souvenir using her French bank-issued Visa credit card.

- Result: My U.S. processor handles the sale. The French bank issued the card. I am charged the fee.

Example 2: The E-commerce Sale My online business sells digital products. A customer in Hong Kong buys a subscription using his Hong Kong-issued Visa card.

- Result: My online payment gateway (a U.S.-based acquirer) processes the sale. The Hong Kong bank issued the card. I am charged the fee. This charge shows up even though the item was digital and no physical goods crossed a border.

Example 3: The Student Card A university student lives in my town for four years. She still uses a Visa debit card issued by her family's bank in Mexico. She buys groceries from my store.

- Result: The card is foreign-issued. I am charged the fee. Even though she lives here, the card's origin is the trigger.

Because this is such a specific rule, I might only see this cost once in a great while. If my business is in a travel hotspot or sells internationally online, however, I will see this particular charge often.

Does the ISA Fee Apply to Debit Cards?

Yes, I need to know that this assessment applies to both credit and debit Visa cards. As long as the card—credit or debit—is issued by a bank outside the United States, the fee is triggered. I cannot accept an international Visa debit card to avoid the charge.

I also note that while the Visa International Service Assessment is the name for Visa's charge, other card networks have similar costs for foreign-issued cards. Mastercard and Discover both have their own versions of this international assessment. I will get to those later.

How Much Does the Visa ISA Fee Cost? (Current Rates)

When I talk about the cost, I need to be precise. The ISA fee is made up of several parts, which can quickly add up and surprise my total effective rate.

The Standard ISA Fee Percentage

As of the last rates I saw, the standard ISA Fee percentage is 1.00 percent of the transaction volume.

This 1.00% is high compared to many other assessment fees. For example, Visa’s standard fees for U.S.-issued cards are much lower.

Crucial Detail: The ISA charge can change slightly if the payment is settled in a currency other than U.S. Dollars (USD). Most U.S. merchants settle in USD, so the 1.00% rate is typical. If I have a setup that allows for multi-currency processing, the rate may adjust a little, though it still stays close to this percentage. If I am dealing with many different currencies, it's wise to review my processor's specific guidelines for currency conversion and settlement.

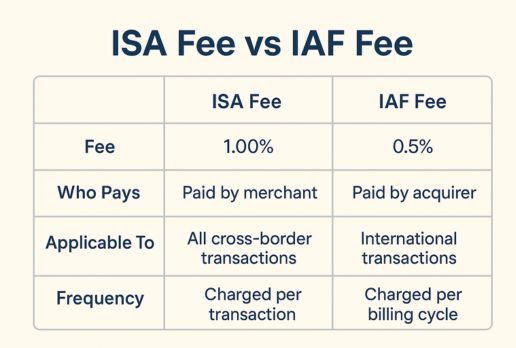

ISA Fee vs. IAF Fee: Understanding the Difference

Here is where the fees begin to stack up. When I accept an international card, I am paying two major international assessments to Visa.

The second fee is called the International Acquirer Fee (IAF).

Note this: Both the ISA and the IAF are charged under the exact same condition—using a non-U.S. issued Visa card. They are two separate charges for the same service.

Here is the comparison based on recent published rates:

- The International Service Assessment (ISA): 1.00 percent on international transaction volume.

- The International Acquirer Fee (IAF): 0.45 percent on international transaction volume.

So, for any single international Visa card payment, the total international assessment cost is roughly 1.45 percent (1.00% + 0.45%) before any other fees are even considered.

Let’s use a simple example to show the math. Say I process a $250 transaction from an international customer:

- ISA Fee: $250 x 1.00% = $2.50

- IAF Fee: $250 x 0.45% = $1.13

- Total International Assessment (Visa): $3.63

That is $3.63 just in network assessments, separate from all other costs.

The Full Cost Picture

It is important to remember that this 1.45% total assessment is only part of my processing cost. This charge is on top of everything else.

My final cost for that $250 international transaction will include:

- Visa International Service Assessment (ISA): 1.00%

- International Acquirer Fee (IAF): 0.45%

- Visa Standard Dues & Assessments: An additional fee (about 0.13% to 0.14%) charged on every transaction, domestic or international.

- Interchange Fees: This is the biggest part of the charge. The customer's foreign bank sets this rate, and it can be high, especially for reward cards.

- Payment Processor's Markup: This is the fee my processor adds on for their service.

When I tally up all five of those layers, a single international card payment can cost my business well over 3 percent or even 4 percent of the sale amount. This high cost is why it is so important to understand where the Visa International Service Assessment fits in.

Locating the Visa ISA Fee on My Merchant Statement

This charge loves to hide. It rarely appears as a perfectly clear line item saying "Visa International Service Assessment Fee." I need to be a detective to find it on my monthly statement.

Common Labels and Names

My processor might use any of these names for the charge, or even a different one:

- Visa International Service Charge

- ISA

- Visa International Service assessment

- International service assessment

- Cross-Border Fee

- Foreign Transaction Fee (less common, but possible)

- Non-U.S. Card Assessment

I always tell my clients: do not trust the title. Trust the numbers. If you see a 1.00% fee applied to only a portion of your Visa volume, you have found it.

Where to Find It Based on Pricing Model

How the charge shows up depends heavily on how my processor bills me. My processor uses one of three main pricing models.

Interchange-Plus Pricing

This is the most transparent method, and the one I recommend for most businesses.

- Where to Look: On my statement, I should look for a section specifically labeled "Card Brand Fees" or "Assessment Fees."

- The Find: The Visa International Service Assessment will be itemized there. I should see the 1.00% rate listed, usually alongside the 0.45% IAF Fee.

- Action: If I am on this plan and cannot find it, I need to scan every line item. If I still can't find it, I call my processor immediately and ask where the charge is located.

Tiered Pricing

This method groups transactions into tiers (Qualified, Mid-Qualified, Non-Qualified), which is not great for clarity.

- Where to Look: I may find it itemized like the Interchange-Plus model, but often it is hidden.

- The Find: International transactions have more assessments (like the ISA and IAF). Because of this, they almost always get bundled into the highest-cost tier, typically the Non-Qualified tier.

- Action: If I see a high percentage rate applied to my Non-Qualified sales, that high rate is almost certainly covering the ISA charge, plus interchange, plus the processor’s markup. It is a confusing system, but the assessment is paid, even if it is not visible by name.

Flat-Rate Pricing (e.g., Stripe, PayPal)

This is simple pricing, but zero transparency on fees.

- Where to Look: I will not find this fee listed anywhere on my statement.

- The Find: The Visa International Service Assessment is absorbed into the single flat percentage rate I pay (e.g., 2.9% + $0.30). My processor collects the fee and pays Visa for me, but the cost is included in my final rate.

- Action: I must accept that I am paying this fee. I just do not get to see the itemized line for it. This is the trade-off for simplicity.

To confirm my total cost, I may need to check several statements. The charge only appears when an international card is used. If I have a slow month for foreign business, it will not show up.

Can a Merchant Reduce or Avoid the Visa ISA Fee?

I have to tell you the hard truth upfront.

Negotiability: The Hard Truth

The Visa International Service Assessment is set by the card network, Visa. This makes the fee:

- Non-Negotiable: I cannot call Visa and ask for a lower rate.

- Non-Avoidable: I cannot switch processors to escape it.

Every payment processor in the U.S. is required to pay Visa this 1.00% rate (plus the IAF) when a foreign card is used. If I accept an international Visa card, I will pay this fee. It is a mandatory cost of global commerce.

However, I can still reduce my overall processing costs. My focus just needs to be smarter.

Strategies for Controlling Overall International Transaction Costs

Since the ISA charge itself is fixed, I need to focus on the one flexible cost on my statement: the processor's markup.

1. Negotiate the Processor Markup

This is the most important item on my entire statement. My processor's markup is the only part of the fee structure that is fully negotiable. It is their profit.

- If I am currently paying a rate of 0.20% + $0.10 for my markup, I can call them and ask for 0.15% + $0.08. Even a small drop here saves me real money across thousands of transactions.

- I can use my total sales volume as my bargaining chip. Processors want large volume businesses.

2. Switch to Interchange-Plus for Clarity

If I am using Tiered or Flat-Rate pricing, I strongly recommend moving to Interchange-Plus.

- It gives me the most transparent view of the ISA charge.

- I see exactly what Visa charges (the ISA) and exactly what my processor charges (their markup). This visibility alone helps me control my expenses better. When I know where every penny is going, I can manage my money far better.

3. Calculate My Effective Rate

I must know my true average cost of acceptance. This number is my "Effective Rate." It helps me decide if I am being overcharged.

My formula for the Effective Rate Percentage is:

$$\frac{\text{Total Fees Paid in a Month}}{\text{Total Sales Volume in a Month}} \times 100 = \text{Effective Rate Percentage}$$

I need to calculate this monthly. If this percentage creeps up, I know I need to investigate my statement for high-cost items like the international service charge, or a rising processor markup.

I always advise clients to evaluate the value of accepting international business against this rate. If I am handling many payments from abroad, I need to ensure my prices are set correctly to absorb this higher cost. Sometimes, the benefits of getting that international sale outweigh the higher fee.

For professionals who are regularly accepting cards from foreign territories, especially those dealing with specific country regulatory issues—for example, if I am considering how international payments might factor into an Australia visa assessment application process—it is critical to have a clear and accurate effective rate calculation. This preparation makes sure I meet all financial requirements without any surprises.

ISA Fee Across Other Card Networks

I want to give you a full picture. Visa is not the only card network that charges an international assessment. Mastercard, Discover, and American Express all have their own versions of this fee. The names are different, but the purpose is the same: they charge me more because the transaction is cross-border.

Mastercard’s Cross-Border Fee

Mastercard calls its equivalent fee the International Cross-Border Fee. It is structured very much like the Visa charge, with two parts that stack:

- Cross-Border Assessment Fee: Applied when the card is issued outside the U.S.

- Acquirer Program Fee: This second fee is applied to U.S. acquirers (my processors) when they process a transaction from a foreign-issued card.

The total cost from Mastercard is competitive with Visa's total stack of 1.45% (ISA + IAF).

Discover’s International Processing Fee

Discover, while having fewer cards in the U.S. market, has a simpler structure. They charge an International Processing Fee for transactions using cards issued abroad. It is often a single, slightly lower rate compared to the stacked fees from Visa or Mastercard, but it still exists and is non-negotiable.

American Express’s International Assessment Fee

American Express (Amex) includes a separate charge called the International Assessment Fee on foreign-issued cards. Amex often charges higher overall rates to merchants than Visa or Mastercard. However, like the others, this specific assessment is mandatory and based on the foreign origin of the customer’s card.

I need to budget for these similar fees, too. If I accept these other card brands, I am paying an international assessment every time a foreign card is used, no matter which card network it is.

Frequently Asked Questions (FAQ)

What does ISA stand for?

ISA stands for International Service Assessment. It is a mandatory fee charged by the Visa card network to U.S. merchants when they accept a credit or debit card that was issued by a bank outside of the United States.

What is the difference between the ISA Fee and the IAF Fee?

The International Service Assessment (ISA) and the International Acquirer Fee (IAF) are both separate assessments charged by Visa on the same international transaction. They stack. The ISA is typically 1.00% and the IAF is typically 0.45%, making the total international assessment 1.45% of the transaction volume, before interchange and processor markups.

Can I negotiate the Visa ISA Fee?

No. The Visa International Service Assessment is set by the card network (Visa) and is mandatory and non-negotiable for all U.S. payment processors. You cannot avoid it by switching processors. Your effort should instead focus on negotiating your payment processor's separate markup.

Does the ISA Fee apply if the customer is physically located in the U.S.?

Yes, absolutely. The fee is triggered solely by the card's origin, not the customer's location. If the customer's Visa card was issued by a foreign (non-U.S.) bank, the ISA fee is charged, even if the customer is standing in your physical U.S. store or shopping on your e-commerce site from a U.S. location.

Does this fee apply to Visa Debit cards?

Yes. The Visa International Service Assessment applies to all non-U.S. issued Visa cards, whether they are credit cards or debit cards.

Conclusion: The Takeaway for Business Owners

The Visa International Service Assessment is a mandatory part of accepting international payments. Visa put it in place to manage the cost and risk of dealing with money that moves between countries. The rate of 1.00% (plus the 0.45% IAF) is fixed. I cannot argue or negotiate this specific charge.

My advice to every business owner is simple:

- Stop searching for a way to avoid the ISA fee. It is a permanent cost of doing business globally.

- Start focusing on my processor's markup. That is where the real savings are. Negotiating that markup, or switching to a transparent Interchange-Plus model, will save me far more money than fighting a fixed assessment.

My time is valuable. I should spend it on running my business, not trying to hunt down fees that Visa will charge me anyway. I need to know the assessment is there, ensure my prices cover it, and keep my eye on the biggest piece of the pie: my processor’s bill.

Go grab your latest merchant statements. See if you can spot the ISA charge or its foreign counterparts from Mastercard and Amex. Let me know if you would like me to help you compare your current processor's rate against a more transparent model, or if you want to look at how these high international fees impact your total yearly revenue.